Hedgebook has developed a Credit Value Adjustment (CVA) module that enables users to inexpensively include CVA/DVA as part of the fair value of their financial instruments as prescribed by IFRS 13.

In line with Hedgebook’s community of users we have deliberately kept the CVA module towards the simpler end of the CVA calculation spectrum. We use the current exposure method which we feel is appropriate for vanilla instruments such as FX forwards, FX options and interest rate swaps for an entity using these instruments for hedging purposes.

The module is broken into the following steps:

- Creating new credit curves (both for the counterparty to the transaction and the company’s own credit).

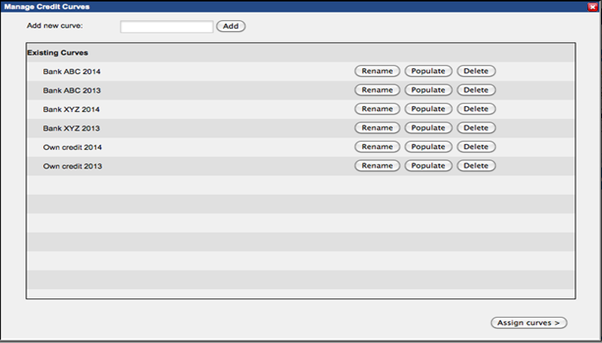

- Managing previously created credit curves

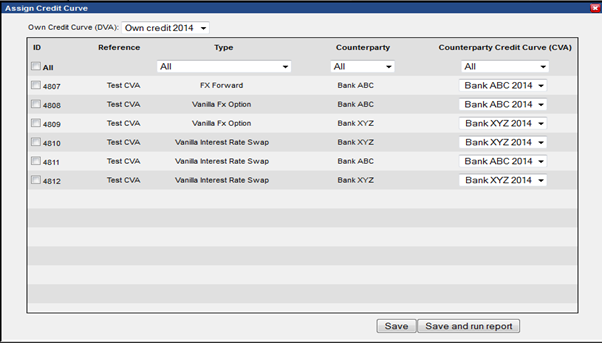

- Assigning credit curves to instruments

- Running the CVA/DVA report

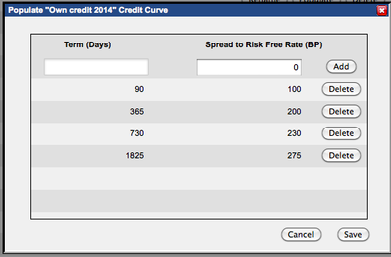

Creating credit curves

The user needs to include at least one data point for Hedgebook to create a credit curve. Hedgebook linearly interpolates/extrapolates as appropriate. The more data points that can be included the better and sources such as treasury advisors, banks, corporate bonds and bank funding costs are all useful sources for determining credit spreads. The user will need to add at least two curves – one to reflect the counterparty to the transaction and one to represent the company’s own credit standing. Hedgebook adds the credit curve to the risk-free curve so that future cashflows can be discounted to present value and compared against the risk-free valuation.

Once the credit curves have been added they are saved and can be amended/deleted as necessary:

The final step before running the report is applying the counterparty credit curves to individual deals as appropriate. All of the curves created by the user are available.

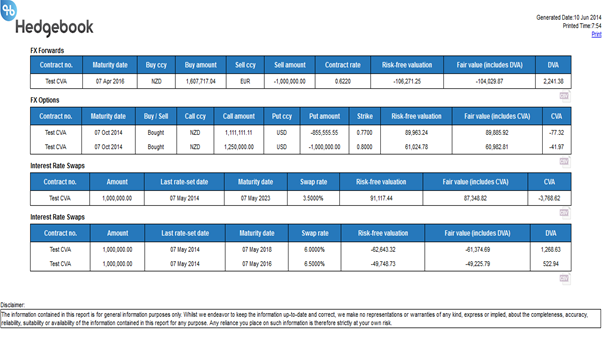

Once the user is satisfied the deals have been correctly assigned with a credit curve, the CVA report can be run. The output of the report is split by instrument type and includes the risk-free valuation as well as the fair value and CVA/DVA amount.

We have focused on providing a relatively simple solution to a new and complex area of financial reporting. For many companies 30 June will be the first time CVA/DVA has been included in the fair value of financial instruments. If CVA is causing you an expensive headache then get in touch because we can help.